by

by You have debt. Maybe it is a credit card. Maybe it is a student loan, a car payment, or three different bills staring at you every time you open your banking app. You have decided you are done with it, and you want it gone.

But then you Google “how to pay off debt” and suddenly you are staring at two different strategies with two very different approaches — and nobody seems to agree on which one is better.

The Debt Snowball says s start with your smallest debt first. The Debt Avalanche says attack the highest interest rate first. Both work. Both have passionate supporters. And choosing the wrong one for your personality could be the difference between finishing debt-free and quietly giving up six months in.

This post is going to settle the debate once and for all — not by picking a winner, but by showing you exactly which method is right for you specifically.

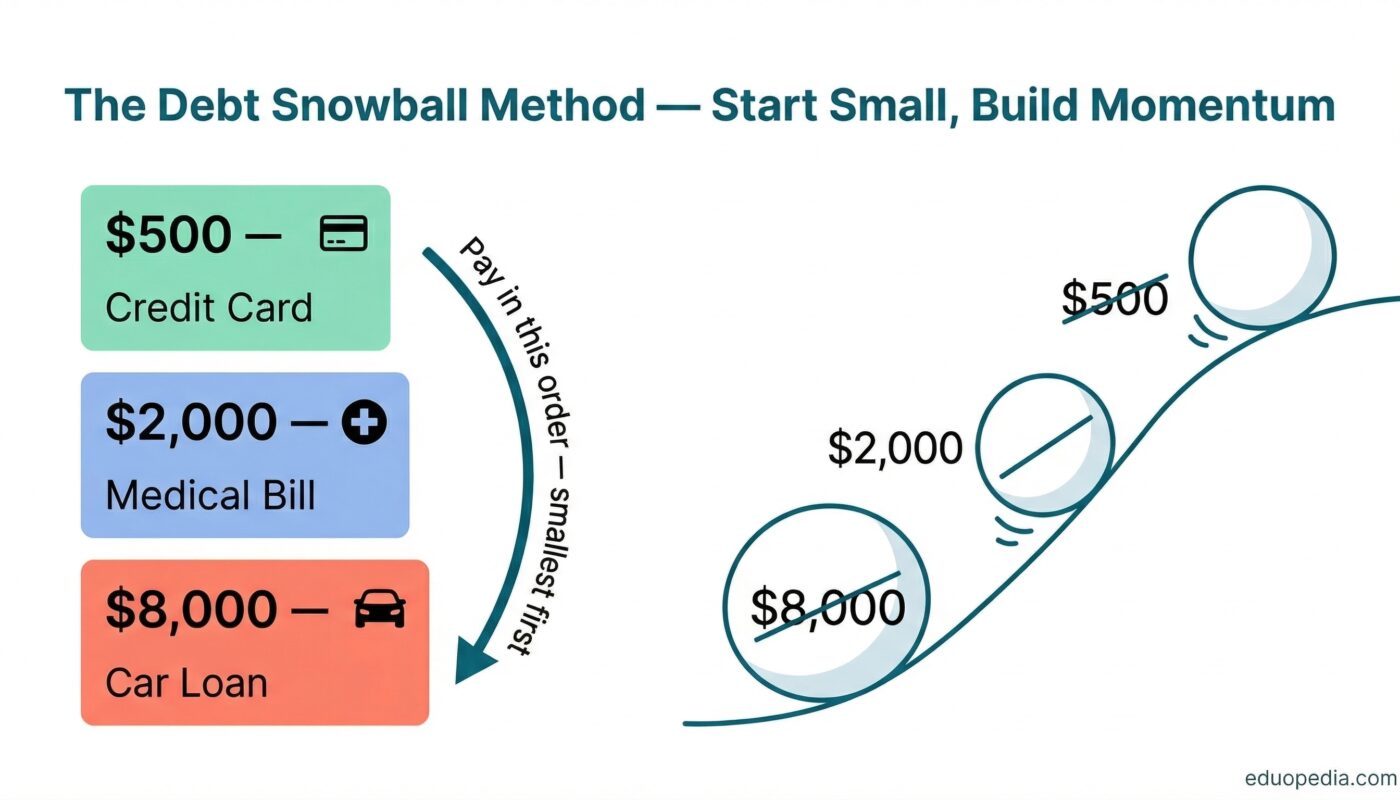

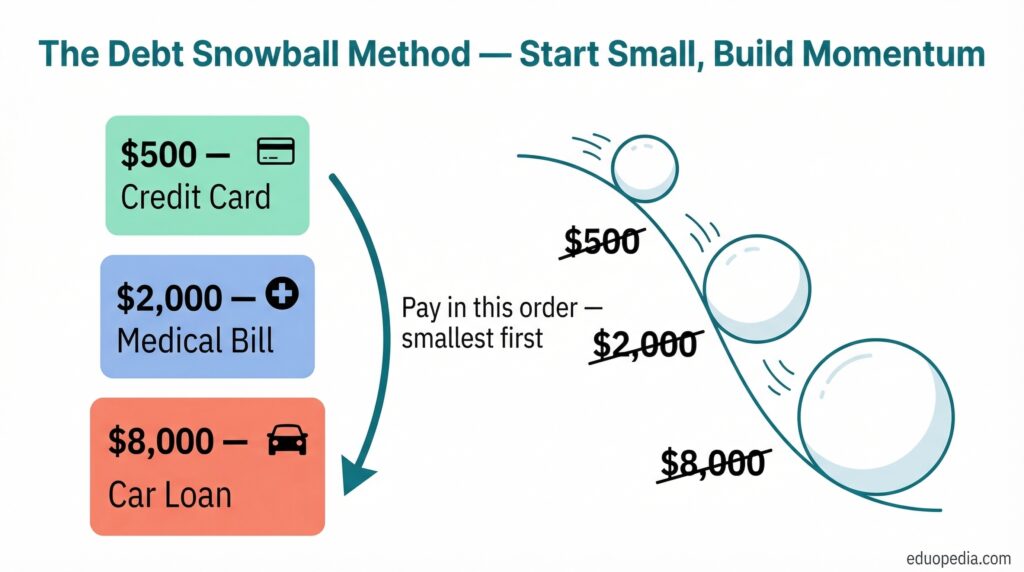

What Is the Debt Snowball Method?

The Debt Snowball method was made famous by personal finance author Dave Ramsey. The concept is simple and deeply psychological.

Here is exactly how it works:

Step 1 — List all your debts from the smallest balance to the largest balance. Ignore the interest rates completely for now.

Step 2 — Make the minimum payment on every single debt except the smallest one.

Step 3 — Throw every extra dollar you can find at the smallest debt until it is completely gone.

Step 4 — Once that smallest debt is paid off, take the money you were paying on it and add it to the minimum payment of your next smallest debt. This is the snowball rolling and picking up speed.

Step 5 — Repeat until every debt is gone.

Here is a simple example. Say you have three debts:

- Credit Card A — $500 balance at 19% interest

- Medical Bill — $2,000 balance at 0% interest

- Car Loan — $8,000 balance at 7% interest

With the Snowball method, you attack Credit Card A first because it has the smallest balance, even though the medical bill has zero interest and the car loan has a lower rate. You pay minimums on the medical bill and car loan, and hammer every spare dollar at that $500 credit card until it is completely dead.

When the credit card is gone, you roll that payment into the medical bill. When the medical bill is gon,e you roll everything into the car loan. By the time you reach your biggest debt, you have a massive payment hitting it every single month — hence the snowball.

The reason this method works so powerfully is not financial. It is psychological. Human beings are wired to respond to visible progress and quick wins. Every time you eliminate a debt — no matter how small — your brain gets a hit of dopamine, your confidence goes up, and your belief that you can actually do this becomes unshakeable.

When people say they tried to pay off debt and failed, it is rarely because they ran out of money. It is because they ran out of motivation. The Snowball method is specifically designed to keep motivation alive.

“The debt snowball works not because of math. It works because of motivation.” — Dave Ramsey

What Is the Debt Avalanche Method?

The Debt Avalanche method is the mathematically optimal approach to paying off debt. Where the Snowball focuses on emotional wins, the Avalanche focuses on numbers and saving the most money overall.

Here is exactly how it works:

Step 1 — List all your debts from the highest interest rate to the lowest interest rate. Ignore the balances completely.

Step 2 — Make the minimum payment on every debt except the one with the highest interest rate.

Step 3 — Direct every extra dollar toward the debt with the highest interest rate until it is completely paid off.

Step 4 — Once that highest-rate debt is gone, roll its payment into the next highest interest rate debt.

Step 5 — Repeat until every debt is eliminated.

Using the same example as before, but now ordered by interest rate:

- Credit Card A — $500 balance at 19% interest ←. Attack this first

- Medical Bill — $2,000 balance at 0% interest ← . Pay the minimum only

- Car Loan — $8,000 balance at 7% interest ← . Pay a minimum only

Interestingly, in this particular example, the Snowball and Avalanche give you the same starting point — the credit card — because it happens to have both the smallest balance and the highest interest rate. But in most real-life situations, the two methods will point you in completely different directions.

Imagine if instead the numbers looked like this:

- Credit Card A — $500 balance at 8% interest

- Personal Loan — $6,000 balance at 24% interest

- Car Loan — $8,000 balance at 7% interest

The Snowball tells you to attack the $500 credit card first because it is the smallest. The Avalanche tells you to ignore that entirely and go straight for the $6,000 personal loan because 24% is destroying you financially every single month you carry it.

That is the core tension between these two methods and why this debate gets so passionate among personal finance people.

💡 Pro Tip: The Avalanche method saves you the most money in total interest paid over the life of your debts. But saving money and staying motivated are two completely different challenges and they require completely different solutions.

Snowball vs Avalanche — Side-by-Side Comparison

| Higher progress feels slow early | Debt Snowball | Debt Avalanche |

|---|---|---|

| Order debts by | Smallest balance first | Highest interest rate first |

| Extra payments go to | Lowest balance debt | Highest APR debt |

| First win comes | Quickly — small debts die fast | Slowly — may take longer |

| Total interest paid | More — not interest optimized | Less — mathematically optimal |

| Best for | Motivation-driven people | Discipline-driven people |

| Risk of quitting | Lower — quick wins keep going | Higher — progress feels slow early |

| Recommended by | Dave Ramsey | Most financial economists |

A Real Numbers Example — Which Saves More?

Let us use a realistic debt scenario to illustrate the actual numerical difference between these two methods.

Your debts:

- Credit Card — $3,000 balance at 22% APR — Minimum payment $60

- Personal Loan — $7,000 balance at 14% APR — Minimum payment $140

- Student Loan — $15,000 balance at 6% APR — Minimum payment $166

Extra money available to throw at debt each month: $300

Total monthly payment: $666

With the Debt Snowball — attack the credit card first because it is the smallest balance:

You direct your entire $300 extra, plus the $60 minimum, to the credit card — a total of $3,60, hitting it every month. The credit card gets paid off in approximately 8 months. You then roll that $360 into the personal loan, along with its $140 minimum, for a total of $500 per month — attacking the personal loan. The personal loan is gone roughly 20 months after you started. Everything then rolls into the student loan. Total time to complete debt freedom: approximately 38 months. Total interest paid across all three debts: approximately $4,400.

With the Debt Avalanche — attack the credit card first because it also happens to be the highest APR at 22%:

In this specific example, the starting point is identical to the Snowball. However, because you always pivot to the next-highest interest rate — the personal loan at 14% before the student loan at 6% — the Avalanche method squeezes out slightly less total interest paid over the full period. Total time to complete debt freedom: approximately 36 months. Total interest paid: approximately $3,900.

The real-world difference: approximately $500 saved and 2 months faster with the Avalanche.

Now here is the honest conversation that needs to happen. That $500 is real money, and those 2 months matter. But they only matter if you actually finish. If the Snowball method keeps you motivated enough to cross the finish line and the Avalanche leaves you burnt out and defeated after 12 months of slow progress, the Snowball saved you $3,900 in total interest, not lost you $500.

The math favours the Avalanche. Psychology often favours the Snowball. Your job is to figure out which one you are.

Which Method Is Right for YOU?

Here is the honest answer that most finance articles are too afraid to give you — the best debt payoff method is the one you will actually stick with for 2, 3, or 4 straight years without quitting.

But to help you decide, ask yourself these questions honestly.

Choose the Debt Snowball if:

- You have struggled to stick with financial plans in the past

- You need to see visible progress quickly to stay motivated and on track

- You have several small debts that you could realistically eliminate within the first few months

- The emotional weight of debt affects your mental health, and you need some early relief

- You are someone who responds well to checking things off a list and celebrating wins

- You have never successfully paid off a significant debt before, and you need a confidence-building experience first

- Your income is unpredictable, and having fewer monthly debt obligations sooner gives you breathing room

Choose the Debt Avalanche if:

- You are highly disciplined and do not need emotional rewards to stay committed to a plan

- You are comfortable playing a longer game in exchange for saving the most money possible

- Your highest interest rate debts are also relatively small balances, which means you will still get early wins

- You have a stable income and are not at risk of an emergency completely derailing your plan

- You have successfully followed long-term financial plans before, and you trust yourself to stay the course

- Knowing you are paying unnecessary interest every month genuinely frustrates you enough to use it as motivation rather than discouragement.t

- You have a partner or accountability system that will keep you on track even when progress feels invisible.le

There is no shame in either answer. Choosing the Snowball is not admitting weakness. Choosing the Avalanche does not prove you are smarter. It is simply about knowing yourself well enough to pick the tool that fits the way your brain actually works.

The Hybrid Approach — Getting the Best of Both

You do not have to choose one method and follow it religiously for the entire journey. Many of the most successful debt-payoff stories involve a hybrid approach that combines the psychological benefits of the Snowball method with the financial efficiency of the Avalanche method.

Here is how the hybrid works in practice:

Phase 1 — The Quick Win Phase.

Look at your debt list and identify your one or two smallest debts. Eliminate them as fast as humanly possible. Do not worry about interest rates for now. This phase is purely about momentum. Getting one or two debts completely off your list — watching those accounts hit zero — changes something in you. The goal suddenly feels possible. This phase should take no longer than two to three months.

Phase 2 — Switch to Avalanche Mode.

Once you have your early wins locked in and your motivation is running high, pivot your strategy. From this point forward, you attack debts purely by interest rate from highest to lowest. You now have the emotional confidence of the Snowball combined with the financial discipline of the Avalanche working together.

Phase 3 — The Unstoppable Momentum Phase.

As each debt disappears, your available payment grows larger and larger. By the time you reach your final debt,s you are throwing a massive combined payment at them every month. The end accelerates dramatically. What felt like a decade of debt starts to disappear in years. Then in months.

This hybrid approach works especially well for people who have one or two small debts alongside larger, higher-interest debts. Knock out the small ones in month one or two for the confidence boost, then pivot to being completely ruthless about interest rates for the rest of the journey.

Common Mistakes People Make With Both Methods

People who struggle to pay off debt using either method almost always make one of these five mistakes. Knowing them in advance puts you miles ahead.

Not building a small emergency fund first.

This is the single biggest killer of debt payoff, and it is completely avoidable. Without at least $500 to $1,000 sitting in a separate savings account, the first unexpected expense — a car repair, a medical bill, a broken appliance, a vet visit — sends you straight back to the credit card you just paid off. Before you aggressively attack debt, put a small emergency buffer in place first. It feels counterintuitive to save before paying off debt, but it protects everything you are about to build.

Continuing to add new debt while paying off old debt.

You cannot drain a bathtub with the tap still running. If you are paying off credit card debt while still using the credit card for non-essential purchases,s you are working directly against yourself. While you are in active debt payoff mode, pause or freeze the cards. Not forever — just until the balance is gone. This one change alone can cut your payoff timeline in half.

Only ever paying the minimum paymentLenders carefully design minimum payments

Minimum payments are carefully designed by lenders to keep you in debt for as long as possible while you pay as much interest as possible. Paying only the minimum on a $3,000 credit card balance at 22% APR can take well over a decade to clear and cost you more in interest than the original purchase was worth. You must throw extra money at your target debt every single month — even if that extra is just $30 or $50 to begin with.

Missing one payment, then quitting completely.

Life happens, and at some point during a multi-year debt payoff journey, you will miss a month. An unexpected bill will arrive. A difficult week will derail your routine. That is a setback, ck, and setbacks are completely normal and survivable. The people who become debt-free are not the ones who never stumble. They are the ones who stumbled and got straight back on track the following month without guilt, without drama, and without using the stumble as an excuse to quit entirely.

Not tracking progress visibly.

Debt payoff is a long game measured in years, and motivation naturally fades when the finish line feels invisible. Keep a simple debt tracker somewhere you will see it every single day — a spreadsheet, a notebook, a printed chart on your fridge. Update it every month. Watching the numbers shrink month after month is one of the most powerful motivational tools available to you,u and it costs absolutely nothing to set up.

Your Complete Debt Payoff Action Plan

Stop reading about paying off debt and start actually doing it. Here is your complete action plan to begin this week:

This week:

- Write down every single debt you owe — credit cards, personal loans, student loans, medical bills, car payments, everything

- Next to each debt, bt write down the current balance, the interest rate, and the minimum monthly payment

- Add up the total amount you owe, so you know the exact number you are working with

- Decide whether you are using the Snowball, the Avalanche, or the Hybrid approach

- Identify at least one area in your budget where you can free up extra money to throw at debt — a subscription to cancel, a habit to pause, an income stream to add

This month:

- Set up automatic minimum payments on every single debt so you never accidentally miss one

- Direct every extra dollar to your chosen target debt on payday before you have the chance to spend it

- Create a simple debt tracker and stick it somewhere visible in your home

- Tell one person about your debt payoff plan for accountability

Every month from here:

- Review your debt balances on the first of each month

- Celebrate every debt that hits zero — this matters more than it sounds

- Roll each cleared payment immediately into the next target debt

- Adjust your strategy if your financial situation changes significantly

You do not need to be aggressive from day one. Starting with an extra $50 per month is infinitely better than waiting until you can afford an extra $500. The single most important step in this entire process is the first one — writing down exactly what you owe and making the decision that you are going to do something about it,t starting today.

Final Thoughts

Both the Debt Snowball and the Debt Avalanche are proven strategies used by millions of ordinary people to eliminate debt and build real financial freedom. One is not universally superior to the other. The Avalanche saves more money on paper. The Snowball keeps more people in the game long enough to actually finish.

What matters infinitely more than which method you choose is that you choose one today and take the very first step.

Write down your debts. Pick your strategy. Make one extra payment this month.

Because every month you spend thinking about paying off debt instead of actually paying it off is another month of interest charges quietly draining your future, another month of financial stress sitting on your chest, and another month of delayed freedom that you absolutely deserve.

Your debt-free life is not a fantasy. It is a math problem with a solution. You just found the method. NodNo, oo use it.

📌 Found this helpful? Save this post to your Pinterest finance board and share it with someone who is trying to figure out where to start with their debt. It might be exactly what they needed to read today. eduopedia.com

Tags: debt snowball vs avalanche, debt payoff methods, how to pay off debt fast, personal finance, debt-free journey, debt snowball method, debt avalanche method, paying off debt faster, budgeting tips, financial freedom, get out of debt, debt payoff plan