by

by Most people don’t budget because budgeting feels complicated. You imagine spreadsheets, calculators, and tracking every single rupee or dollar you spend on coffee. It sounds exhausting before you even start.

But what if budgeting could be as simple as splitting your money into just three buckets?

That’s exactly what the 50/30/20 rule is. No complicated apps required. No financial degree needed. Just one clear framework that tells you where your money should go — every single month.

By the end of this post, you’ll know exactly how to use it, whether it works for your situation, and how to get started today.

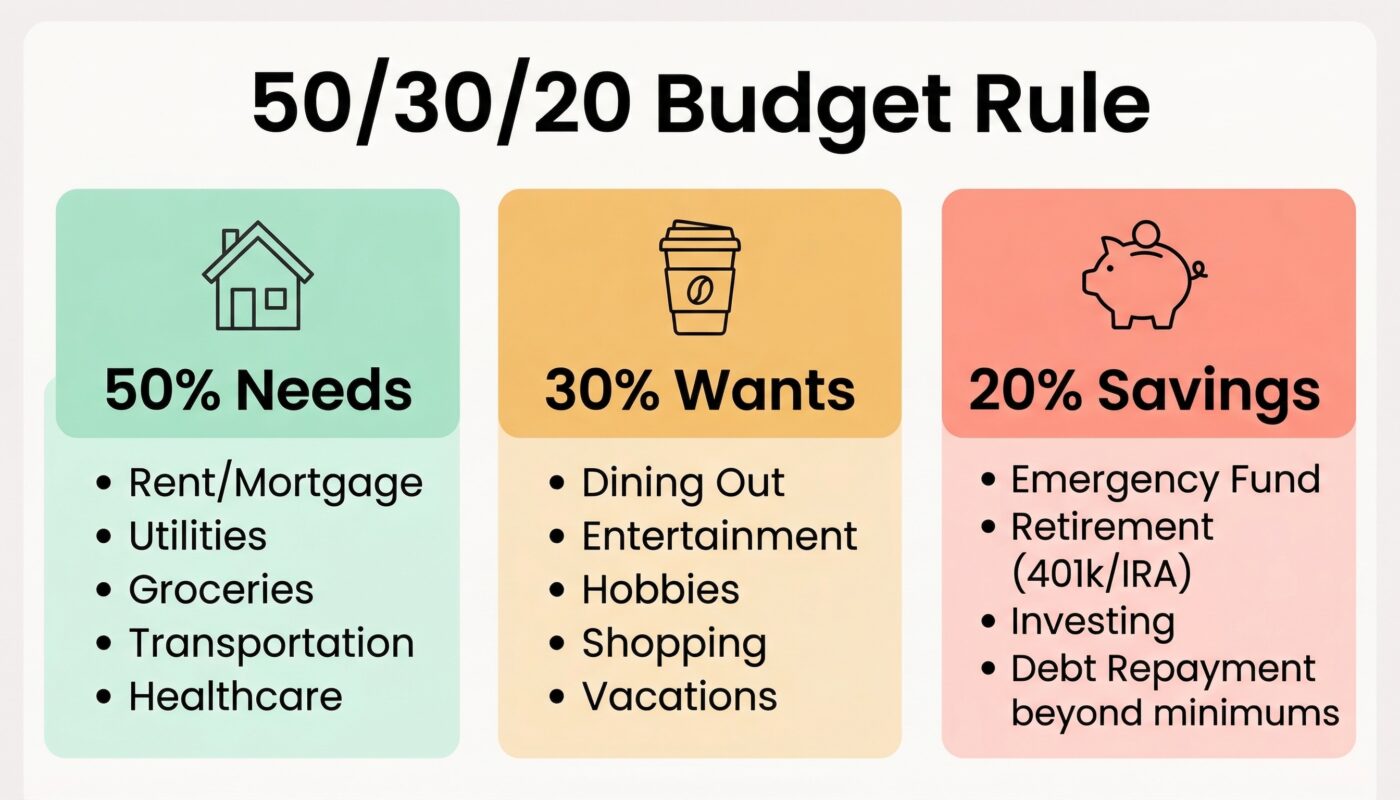

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a budgeting method that divides your after-tax income into three categories:

- 50% goes to Needs — the things you absolutely must pay for to live

- 30% goes to Wants — the things that make life enjoyable but aren’t essential

- 20% goes to Savings and Debt Repayment — your financial future

That’s it. Three numbers. Three buckets. One clear plan.

U.S. Senator Elizabeth Warren popularised the rule in her book All Your Worth as a straightforward way for ordinary people to manage money without getting lost in the details. It has since become one of the most recommended budgeting frameworks in personal finance — and for good reason.

“A good budget isn’t about restricting your life. It’s about giving every dollar a direction.”

The 50/30/20 Rule at a Glance

| Category | % of Income | What It Covers | Example ($5,000/mo) |

|---|---|---|---|

| Needs | 50% | Rent, groceries, utilities, transport, insurance, minimum debt payments | $2,500 |

| Wants | 30% | Dining out, subscriptions, travel, hobbies, entertainment | $1,500 |

| Savings | 20% | Emergency fund, investments, retirement, extra debt payoff | $1,000 |

Breaking It Down: What Goes Where?

50% — Needs (The Non-Negotiables)

Needs are the expenses you cannot avoid. If you stopped paying for them, your life would face serious consequences — you’d lose your home, go hungry, lose your job, or face legal trouble.

Here’s what counts as a Need:

- Rent or mortgage payments

- Groceries (basic food, not restaurant meals)

- Utilities — electricity, gas, water, internet

- Transportation — fuel, public transport, or car payments

- Health insurance and essential medications

- Minimum debt payments (credit cards, student loans)

- Basic clothing and household supplies

What does not count as a Need? Your Netflix subscription. Dining out. The gym membership you rarely use. Those belong in the next bucket.

💡 Pro Tip: If your needs exceed 50% of your income, don’t panic — this is very common, especially in high cost-of-living cities. We’ll cover what to do in that situation later in this post.

30% — Wants (The Good Stuff)

Wants are expenses that improve your quality of life but aren’t survival-level necessities. This is the category most people either overspend on without realising it, or feel guilty about when they don’t need to.

Wants include:

- Dining out and takeaways

- Streaming services (Netflix, Spotify, etc.)

- Gym memberships and fitness classes

- Weekend trips and holidays

- Hobbies — books, games, sports gear

- Shopping for non-essential clothing or gadgets

- Entertainment — movies, concerts, events

The key distinction: a Need is what you must have. A Want is what you choose to have.

For example, you need transportation, but choosing a luxury car over a budget one? That extra cost is a Want. You need food, but eating at a restaurant three times a week instead of cooking at home? That’s a Want.

⚠️ Important: The 30% category is NOT something to be ashamed of. Life is meant to be enjoyed. The 50/30/20 rule deliberately gives you permission to spend on things you love — as long as it stays within the limit.

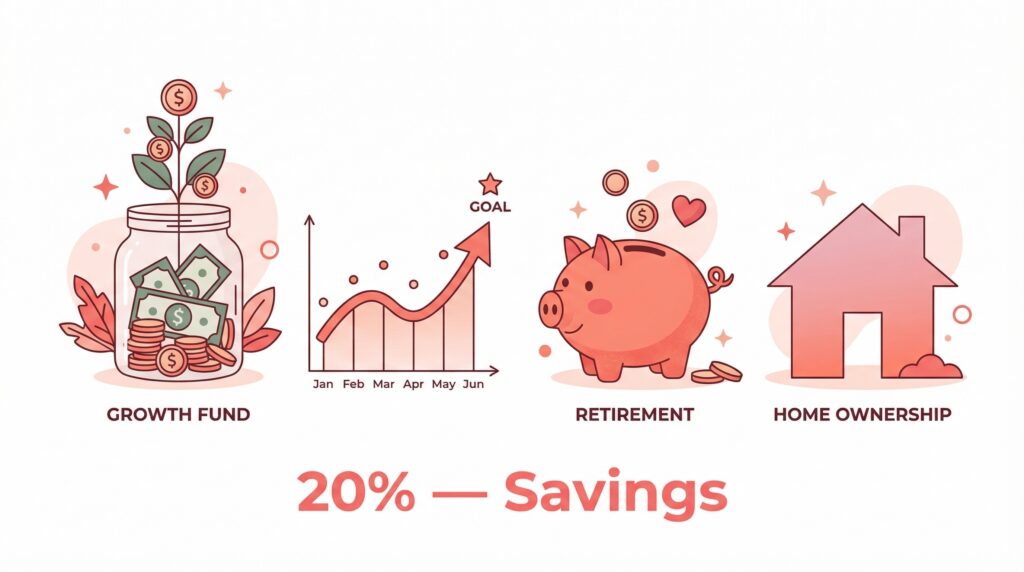

20% — Savings and Debt Repayment (Your Future Self)

This is the category that separates people who build wealth from people who wonder where their money went.

The 20% category covers:

- Emergency fund (target: 3–6 months of expenses)

- Retirement contributions (401k, pension, or equivalent)

- Investments — stocks, index funds, real estate

- Extra debt payments above the minimum

- Saving for a specific goal — house deposit, car, education

Why does this matter so much? Because without intentional saving, most people reach their 40s and 50s with almost nothing set aside. The 20% rule ensures you’re always paying your future self first — before the money disappears into spending.

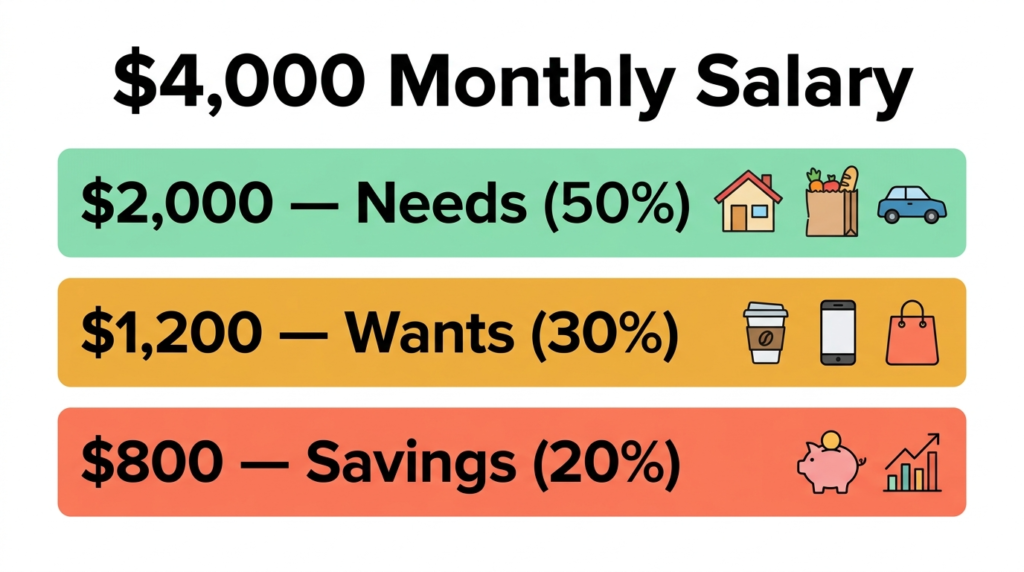

Real-Life Example: How It Works with Numbers

Let’s make this concrete. Say your monthly take-home pay (after taxes) is $4,000.

50% Needs = $2,000 Rent: $1,200 | Groceries: $400 | Utilities: $150 | Transport: $250

30% Wants = $1,200 Dining out: $300 | Subscriptions: $100 | Shopping: $400 | Hobbies: $400

20% Savings = $800 Emergency fund: $300 | Retirement: $300 | Extra debt payoff: $200

Clean. Simple. No financial degree required.

How to Calculate YOUR 50/30/20 Budget

Follow these four steps to set up your own budget:

Step 1: Find your after-tax monthly income. This is your take-home pay — what actually hits your bank account after taxes and deductions. If your income varies month to month (freelancers, this is for you), take an average of your last 3 months.

Step 2: Calculate your three numbers. Multiply your take-home income by 0.50, 0.30, and 0.20 to get your three budget targets.

Step 3: Track what you currently spend. Look at your last month’s bank and credit card statements. Categorise each expense as a Need, Want, or Saving. Most people are surprised — and a little horrified — by what they find.

Step 4: Adjust until your spending matches your targets. If your Wants are eating up 45% of your income, you know where to cut. If you’re saving only 5%, you know what needs to grow. The numbers show you the truth — then you decide what to do about it.

What If 50/30/20 Doesn’t Fit My Life?

Here’s where I’ll be real with you: the 50/30/20 rule is a guideline, not a law. Life is messy, and it doesn’t always fit neatly into three tidy percentages.

“My needs are more than 50%”

This is extremely common — especially if you live in an expensive city, have children, or are managing student debt. If your needs exceed 50%, try borrowing from the 30% (Wants) category first, not the 20% (Savings) category. Protect your savings as much as possible. And look for ways to reduce high fixed costs over time — negotiating rent, refinancing loans, or moving to a less expensive area.

“I have a lot of debt — should I still save 20%?”

Yes — but tweak the formula. A good approach is to split your 20% between savings and aggressively paying down debt. Even saving a small emergency fund ($500–$1,000) before attacking debt is important, because without it, every unexpected expense sends you right back to borrowing.

“I have a low income — 20% savings isn’t realistic”

Start with whatever percentage you can. Even 5% is better than 0%. The 50/30/20 rule gives you a target to work toward — not a standard to shame you with. As your income grows or your expenses shrink, you can gradually increase your savings rate.

💡 Remember: Any rule that helps you spend with intention is better than no rule at all. Adjust the percentages to fit your reality — what matters most is the habit of allocating your money before you spend it.

The Biggest Benefits of the 50/30/20 Rule

- It’s dead simple. Anyone can calculate three percentages. No complicated categories, no exhausting tracking systems.

- It permits you to enjoy your money. The 30% Wants bucket means you don’t have to feel guilty for having fun — as long as you stay within it.

- It automatically builds savings into the system. The 20% isn’t an afterthought — it’s built right into your plan from day one.

- It’s flexible enough for real life. The percentages are starting points, not rigid rules carved in stone.

- It works for any income level. Whether you earn $1,500 or $15,000 a month, the same proportions apply.

Common Mistakes to Avoid

Confusing Wants for Needs. Be brutally honest with yourself. A streaming service is not a Need. A gym membership is not a Need. Mislabeling Wants as Needs is how the 50% bucket quietly overflows.

Treating savings as optional. The 20% category is not “what’s left over.” It should come out first — ideally via automatic transfer on payday, before you can spend it.

Giving up if the first month is messy. Budgeting is a skill. Your first attempt will be imperfect. Track, adjust, and try again next month.

Not revisiting the budget when life changes. A raise, a new baby, moving cities — any major life change means your budget needs to be recalculated.

Your Action Plan: Start Today

Here’s how to put this into practice right now, in less than 30 minutes:

- Open your bank app or statement from last month

- Add up your total take-home income

- Calculate 50%, 30%, and 20% of that number

- Go through your expenses and label each one: Need, Want, or Saving

- Compare your actual spending to your targets

- Identify the one biggest area where you can cut — and do it

- Set up an automatic transfer to savings on payday

That’s it. Seven steps. You don’t need a perfect system to start — you need to start.

“You don’t have to be great to get started, but you have to get started to be great.”

Final Thoughts

The 50/30/20 budget rule works because it’s simple enough to use. Most financial systems fail not because they’re wrong, but because they’re too complicated to stick with when life gets busy.

This rule doesn’t ask you to track every coffee or obsess over every expense. It asks you to do one thing: make sure your money is moving in the right direction — toward security, toward enjoyment, and toward a future you’re actually building.

Start this month. The best time to build a budget was ten years ago. The second-best time is right now.

📌 Found this helpful? Save this post to your Pinterest finance board so you can refer back to it anytime. And share it with a friend who’s been putting off getting their budget sorted — it might be the nudge they need.

Tags: budgeting tips, 50/30/20 rule, personal finance, money management, saving money, budget for beginners, financial planning